Financial Account Status Lifecycle

Learn how to manage your Financial Accounts throughout the lifecycle of your customers

Managing the account status lifecycle is important in financial systems for several reasons:

-

Risk Management: Actively managing financial account status — including suspending, restricting, or closing financial accounts when needed — helps mitigate potential fraud or unauthorized transactions. If a credit or charge financial account remains active without oversight, there's a risk that someone could continue to use it without the account holder's knowledge, especially if there's a high balance or extended line of credit.

-

Credit Exposure: Transitioning financial accounts through appropriate status states — from active to suspended, restricted, or charged-off — reduces the lender's exposure to risk. Managing status ensures no further credit issuance occurs at the right point in the lifecycle, which is crucial for managing overall credit limits and outstanding balances and keeping risk within acceptable boundaries.

-

Credit Score Impact: For consumers, changes in financial account status can affect their credit score. Status transitions that affect available credit — such as restricting a financial account with a significant credit limit — can increase credit utilization ratio (credit used vs. available credit), which can impact their score negatively. Understanding when and why financial accounts move through status changes can help both lenders and consumers manage their credit health effectively.

-

Compliance: Financial institutions must comply with regulatory requirements, including transitioning financial accounts to appropriate statuses when they are inactive for a certain period or involve suspicious activity. Properly tracking financial account status supports reporting and meeting legal obligations in areas like money laundering and consumer protection.

-

Consumer Rights and Transparency: Clear financial account status management ensures that consumers can track and manage their credit/charge activity properly. Status changes — from active to suspended, restricted, or closed — provide consumers with visibility into the state of their financial account relationship, helping them resolve outstanding balances and prevent unexpected charges.

Status Definitions

- PENDING: This status indicates that the financial account is linked to a credit or charge product but has not yet been fully configured. The account is in the process of setup and cannot be used for transactions until it moves to the next stage.

- OPEN: The account is fully set up and operational. It can now be used for financial transactions, and all features of the associated product are accessible to the entity.

- SUSPENDED: Certain restrictions or limitations are now imposed, most notably that card swipes will not be authorized. These restrictions may be temporary, such as for a specific investigation, or part of an ongoing issue that needs resolution. Transactions may be limited or suspended until the issue is resolved or the suspension is lifted.

- CLOSED: This is a terminal state for the financial account. No further transactions can be processed, and the account is effectively deactivated. Any associated product or credit line is no longer active, and the account is closed to any future use.

The following transaction types will be permitted based on the status the account is in:

| Activity | Allowed For |

|---|---|

| Book transfer | OPEN,SUSPENDED |

| ACH Debit Origination | OPEN,SUSPENDED |

| ACH Credit Origination | OPEN |

| ACH Credit Receipt | OPEN, SUSPENDED |

| Management Operation | OPEN, SUSPENDED |

| External Payment - Deposit | OPEN, SUSPENDED |

| External Payment - Withdrawal | OPEN |

| Card Authorizations | OPEN, SUSPENDED(force posts only) |

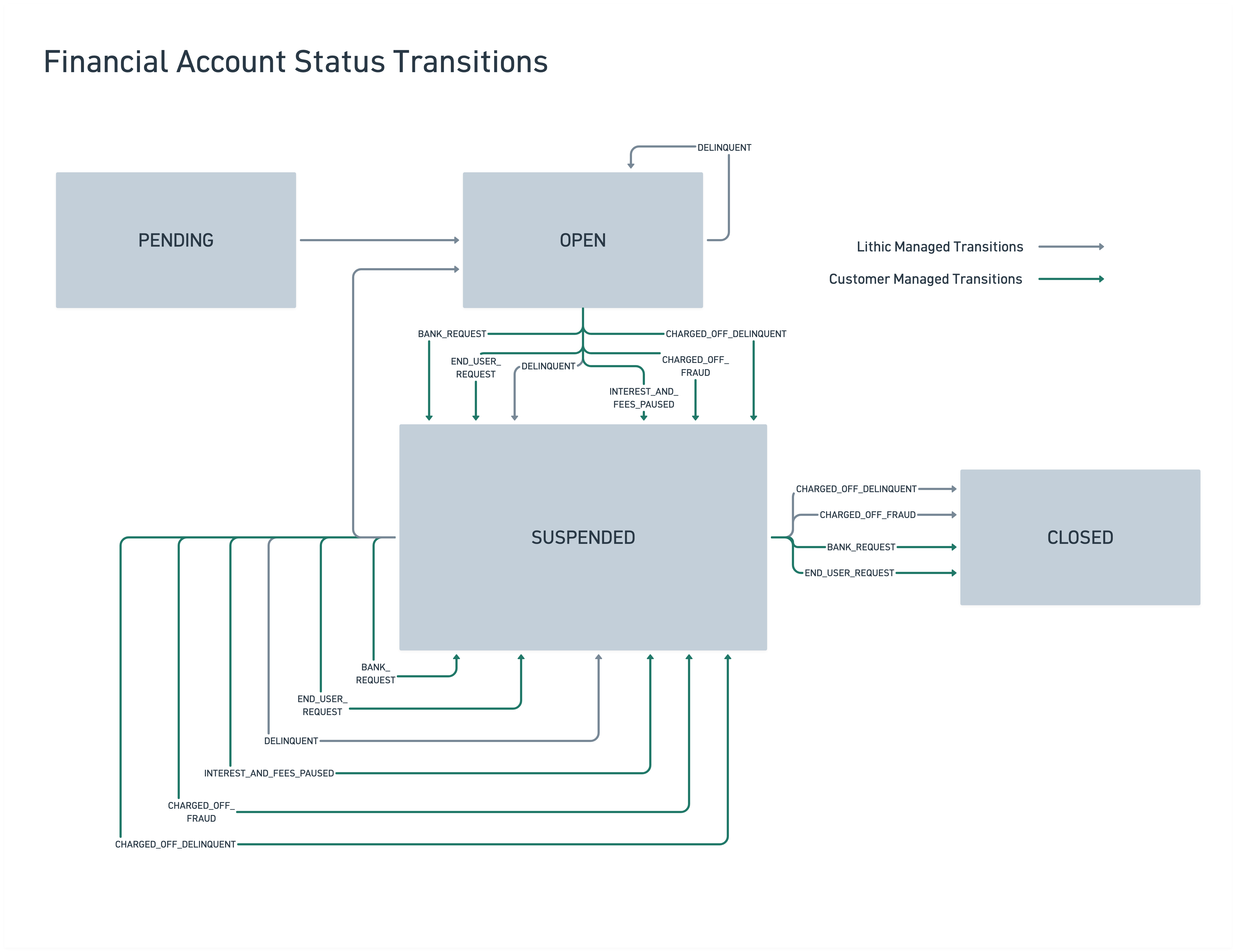

Changing the Status of a Financial Account

The below diagram shows a complete picture of valid transitions for Financial Account status and substatus

statusis indicated by the large gray boxessubstatusis indicated by the arrows

Customer Managed Transitions are completed using the Update Financial Account Status endpoint

Notes on Financial Account Status transitions

Only Credit Financial Accounts use the PENDING status. When Credit Financial Accounts are assigned a Credit Product, Lithic will transition them to OPEN

- See one of our Credit Quick Start guides to learn more

Certain conditions must be met for an account to transition to the CLOSED status. Specifically, the following requirements must be satisfied:

- No outstanding balance: The account must have a zero balance in both the pending and available categories.

- No pending payments: There must be no pending payments, including External Payments or ACH transactions, that have not been processed.

SUSPENDED.INTEREST_AND_FEES_PAUSED will pause all interest and fees on the financial account, without moving it to a charged off state.

Please note that after a Financial Account is moved to

SUSPENDED.INTEREST_AND_FEES_PAUSED, Lithic will no longer manage any state transitions for this financial account until the account is restored toOPEN. Once customers move a financial account fromSUSPENDED.INTEREST_AND_FEES_PAUSEDtoOPEN, Lithic will resume automatic delinquency state transitions.

Charge off workflow

When you move a Financial Account to SUSPENDED.CHARGED_OFF_* (CHARGED_OFF_DELINQUENT or CHARGED_OFF_FRAUD), Lithic manages the downstream charge-off processing through the daily loan-tape build. The steps below happen on the next Loan Tape after the status change.

- Balance write-off: On the next daily loan-tape build after the account enters

SUSPENDED.CHARGED_OFFwith a non-zero balance, the outstanding balance is written off — principal, fees, and interest are each posted as separate loss write-off entries into dedicated charged-off ledger accounts which can be viewed by your program. - Interest and fees stop: From the charged-off period forward, no interest accrues and no late fees are assessed for the account.

- Auto-collections disabled: From the same period onward, auto-collections are disabled. The account is excluded from automatic payment processing, so no collection attempts are triggered.

- Spend blocked: Because the account's status is

SUSPENDED, card authorizations are declined (force posts are unaffected, per the activity table above). The block persists because a charged-off account cannot transition back toOPEN. - Automatic close: When the balance reaches zero, the daily build automatically transitions the account from

SUSPENDEDtoCLOSED, preserving the charge-off substatus (delinquent vs. fraud) for audit and reporting.

Updated about 2 months ago